0

Fund 1

Fund 2

Fund 3

Fund 4

Contact us

Contact Nuveen

Thank You

Thank you for your message. We will contact you shortly.

Retirement investing

Addressing the retirement conversion challenge: a global perspective

Across the globe, retirement systems are being reshaped in response to demographic and economic pressures. Longer lifespans, declining worker-to-retiree ratios, and the shift from defined benefit (DB) to defined contribution (DC) plans are raising questions about sustainability, access, and long-term security. Retirement plan stakeholders have long focused on the accumulation phase of saving, but increasingly the greater challenge lies in how workers convert their savings into dependable income that lasts through retirement. To address this challenge, a recent TIAA Institute study examined 11 countries’ retirement programs to identify relevant insights and practical applications for U.S. plan sponsors and policymakers.

Key takeaways:

- When retirees are left on their own to convert their savings into income, they rarely do.

- Hybrid systems that blend elements of DB and DC plans offer the strongest potential path forward.

- Integrating guaranteed* income options into plans and removing barriers to access significantly increases adoption.

A changing retirement landscape

Three major forces are driving global reforms. First, rising life expectancy is increasing the number of years workers must fund their retirement. Second, falling worker to retiree ratios are straining pay as you go systems and making future payments feel unstable. Third, the shift from DB plans to DC plans has transferred market, longevity and other risks from institutions to individuals.

These factors are in turn creating a retirement conversion challenge for retirees. While some retirees value the flexibility of managing their own accounts in a DC plan, others may be unsure how to safely translate their balances into income. Or, some retirees may underspend out of fear, making retirement less enjoyable, but others might overspend early and face difficult choices later.

Around the world, workers typically have a familiar set of choices for withdrawing their retirement savings. Options can include full or partial lumpsum distributions, programmed term withdrawals, or variable or fixed annuities that offer guaranteed lifetime income.

While these paths appear straightforward, the choice architecture surrounding them can be the defining factor as to whether retirees annuitize their retirement savings. In fact, when annuitization is a voluntary opt-in choice, uptake remains low.

Integrating guaranteed income within the retirement plan fundamentally changes this dynamic. In plan annuities, default retirement income pathways and simplified election processes all help retirees adopt a solution that can lead to a more successful retirement.

The spectrum of choice: from individual to collective

To assess how countries balance risk-sharing and participant choice, the research plotted retirement systems along a spectrum from Individual Choice (IC) to Collective Choice (CC).

IC systems, typically associated with DC plans, feature voluntary participation, broad investment choice and individuals bearing most of the investment and longevity risk.

CC systems, with a starting point close to DB plans, offer narrow individual discretion, emphasize risk pooling, and rely on fiduciary oversight to shield retirees from shocks.

While some countries fall into one of these two categories, a handful take a more balanced approach and offer participants the potential for market growth and flexibility while also helping mitigate risks like longevity.

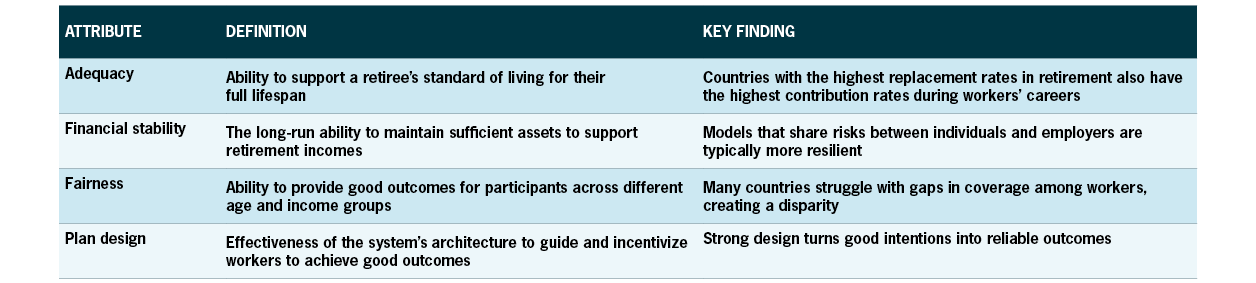

Evaluating retirement systems: a consistent framework

As part of its research, the TIAA Institute developed a standardized framework to evaluate each country’s retirement system across four key attributes, enabling like-for-like comparisons of the various factors that define retirement systems.

In addition to the general findings above, the research identified some high-level lessons from each country. For example, the U.S. was noted for its clear rules on fiduciary oversight, while Japan heavily incentivizes private savings in its system. Elsewhere, Sweden has a flexible retirement age that helps encourage workers to retire later, while Switzerland is noteworthy in how it integrates annuitization as an option for participants.

Some countries have decided upon individual choice or collective choice systems, while others take a more balanced approach and offer market growth with flexibility.

The global move toward hybrid systems

Retirement systems built around DC plans can help workers accumulate savings, offering flexibility and the potential for market‑based growth. DB structures provide guaranteed lifetime income that can help protect retirees from longevity risk retirees from longevity risk but can face sustainability challenges when promised benefits exceed available funding. There is an international trend toward hybrid systems, which offer a way to balance these strengths. The research identified five key elements of successful hybrid programs:

- Universal participation in a high quality plan that also provides retirement income

- Contribution rates that are high enough to fund meaningful retirement income

- Risk-sharing across stakeholders, which supports long term sustainability

- Flexibility and portability that is in-line with worker patterns and preferences

- Fiduciary oversight, plan design and advice that can guide individuals to good decisions

Countries, legislators and providers are already taking steps toward hybrid systems designed to harness the best features of DB and DC plans. Such hybrid systems require a rebalancing of responsibilities and risk burdens between employers, workers and the government.

Trends influencing the move toward hybrid systems

-

Individual Choice countries are introducing more longevity risk-sharing and guaranteed income option

-

Collective Choice countries are shifting more risk to retirees and giving them more choice

-

Legislators are introducing initiatives that promote annuitization (e.g., retirement income covenant in Australia, the SECURE Acts in the U.S.)

-

Product providers are innovating in automated savings conversion, portability, pricing and other ways, depending on their countries’ starting points

The way forward

Building systems that optimize retirement income requires an approach that draws on global experience while adapting to evolving workforce needs. The research provides elements of a blueprint for this new age of retirement systems:

- Hybrid models offer the strongest path forward and represent a promising and sustainable direction for future retirement design.

- Countries vary widely in their approaches, but there are lessons from each that can help inform more effective systems.

- Making retirement income accessible and easy for workers meaningfully increases the likelihood of uptake.

We believe that U.S. legislators and policymakers should prioritize reforms that make guaranteed lifetime income options an integrated part of the retirement planning process. This includes safe harbors for lifetime income providers, support for portability of guarantees, incentives for auto features, and exploration of collective risk sharing to create a stronger, fairer system while honoring individual choice. Policymakers should:

- Remove regulatory barriers to innovation

- Incentivize without mandating

- Embrace the hybrid future

- Act with urgency

Retirement security ultimately depends on getting the conversion moment right. As societies age and DC dominance grows, this challenge will determine whether decades of saving translate into genuine financial independence. The global evidence points clearly toward hybrid systems — frameworks that blend individual flexibility with collective protections and embed guaranteed income into intuitive plan designs. We believe that for the U.S., the path forward is both practical and urgent: design for income, share risks wisely, and make the best outcomes the easiest ones to choose. The destination is a retirement system where more workers can retire with confidence.

We believe that a successful system needs to leverage the best elements of DB and DC plans to find a balance between the goals of adequacy, financial sustainability and fairness.

Download the full PDF to read more

Continue reading

Explore a principles-based framework for adding guaranteed lifetime income to TDFs without losing sight of their core purpose.

A principled approach

to TDFs with guaranteed

lifetime income

Explore now

A survey of U.S. workers reveals how financial pressures are reshaping savings behavior and what plan sponsors can do to help.

Benefits 2.0 survey:

looking to the future so your

participants can focus on

the present

Explore now

Nuveen makes the case for embedding private market investments within target-date funds to broaden diversification and improve retirement outcomes.

The next frontier

for defined

contribution:

embedding

private assets

Explore now

*Any guarantees are backed by the claims-paying ability of the issuing company. Past performance is no guarantee of future results. Guarantees of fixed monthly payments are only associated with fixed annuities.

**The ability to annuitize is subject to plan rules. Converting/Exchanging some or all of your savings to income benefits (referred to as "annuitization") is a permanent decision. Once income benefit payments have begun, you are unable to change to another option.

There is no guarantee that an investment in a target date fund will provide adequate retirement income at or through retirement and investors can lose money at any stage of investment, even near or after the target date.

Asset allocation and diversification do not ensure a profit or protect against a loss. Be sure to see the relevant prospectus or offering document for full discussion of a target date investment option including determination of when the portfolio achieves its most conservative allocation.

Before investing, carefully consider fund investment objectives, risks, charges and expenses. For this and other information that should be read carefully, please request a prospectus or summary prospectus from your financial professional or Nuveen at 800.257.8787 or visit nuveen.com

This material, along with any views and opinions expressed within, are presented for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as changing market, economic, political, or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. There is no promise, representation, or warranty (express or implied) as to the past, future, or current accuracy, reliability or completeness of, nor liability for, decisions based on such information, and it should not be relied on as such. This material should not be regarded by the recipients as a substitute for the exercise of their own judgment. It is important to review your investment objectives, risk tolerance and liquidity needs before choosing an investment style or manager.

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell or hold a security or investment strategy and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor's objectives and circumstances and in consultation with their financial advisors. Financial professionals should independently evaluate the risks associated with products or services and exercise independent judgment with respect to their clients.

This material does not constitute a solicitation of an offer to buy, or an offer to sell securities in any jurisdiction in which such solicitation is unlawful or to any person to whom it is unlawful to make such an offer. Moreover, it neither constitutes an offer to enter into an investment agreement with the recipient of this document nor an invitation to respond to it by making an offer to enter into an investment agreement.

This material may contain "forward-looking" information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of yields and/or market returns, and proposed or expected portfolio composition. Moreover, certain historical performance information of other investment vehicles or composite accounts managed by Nuveen may be included in this material and such performance information is presented by way of example only. No representation is made that the performance presented will be achieved, or that every assumption made in achieving, calculating or presenting either the forward-looking information or the historical performance information herein has been considered or stated in preparing this material. Economic and market forecasts are subject to uncertainty and may change based on varying market conditions, political and economic developments. Any changes to assumptions that may have been made in preparing this material could have a material impact on any of the data and/or information presented herein by way of example.

Important information on risk

Past performance is no guarantee of future results. All investments carry a certain degree of risk, including the possible loss of principal, and there is no assurance that an investment will provide positive performance over any period of time. Certain products and services may not be available to all entities or persons. There is no guarantee that investment objectives will be achieved. See the applicable product literature for details.

Investors should be aware that alternative investments are speculative, subject to substantial risks including the risks associated with limited liquidity, the potential use of leverage, potential short sales, currency exchange rates, and concentrated investments and may involve complex tax structures and investment strategies. Alternative investments may be illiquid, there may be no liquid secondary market or ready purchasers for such securities, they may not be required to provide periodic pricing or valuation information to investors, there may be delays in distributing tax information to investors, they are not subject to the same regulatory requirements as other types of pooled investment vehicles, and they may be subject to high fees and expenses, which will reduce profits.

Target Date Funds: The principal value of the fund(s) is not guaranteed at any time, including at the target-date. The value of a target date fund will fluctuate and investors may lose money. There is no guarantee the Funds' investment objectives will be achieved. For example, it may not achieve its target allocations and even if it does, the asset allocations may not achieve the desired risk-return characteristics and may result in the fund underperforming other similar funds. The target date is an approximate date when investors may begin withdrawing from the Funds. Target-date funds are actively managed, so the asset allocation is subject to change and may vary from that shown. Also, once the target date has been reached, the Funds may be merged into another with the same asset allocation or possibly another with a more stable asset allocation. For Index Funds, a portfolio that tracks an index is subject to the risk that it may not fully track its index closely due to security selection and may underperform when factoring in fees, expenses, transaction costs, and the size and timing of shareholder purchases and redemptions. Target date funds are typically fund of funds subject to the risks of their underlying funds in proportion to each Funds' allocation. These risks may include those of fixed-income underlying funds risks, such as market risk, credit risk, interest rate/duration risk, call risk, tax risk, political risk, economic risk, and income risk. Typically the value of, and income generated by, fixed income investments will decrease or increase based on changes in market interest rates. As interest rates rise, bond prices fall and as interest rates fall, bond prices rise. The Funds' income could decline during periods of falling interest rates. Income is only one component of performance and investors should consider all of the risk factors for an asset class before investing. Credit risk refers to an issuer's ability to make interest and principal payments when due, as well as the prices of bonds declining when an issuer's credit quality is expected to deteriorate. Equity underlying funds risks are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Non-U.S. investments involve risks such as currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards.

Real estate-related assets are less developed, more illiquid, and less transparent compared to traditional asset classes. Real estate investments are subject to various risks, including but not limited to, fluctuations in property values, higher expenses or lower income than expected, changes in economic conditions, currency values, environmental problems and liability, the cost of and ability to obtain insurance, and risks related to leasing of properties.

Private credit/debt investments, like alternative investments are not suitable for all investors given they are speculative, subject to substantial risks including the risks associated with credit risk, interest rate risk, currency risk, prepayment and extension risk, inflation risk, and risk of capital loss, limited liquidity, the potential use of leverage, potential short sales, concentrated investments and may involve complex tax structures and investment strategies. Credit risk refers to an issuer's ability to make interest and principal payments when due, as well as the prices of loans declining when an issuer's credit quality is expected to deteriorate.

Adjustable-Rate Senior Loans may not be fully secured by collateral, generally do not trade on exchanges, and are typically issued by unrated or below-investment grade companies and therefore are subject to greater liquidity and credit risk. Lower credit debt securities may be more likely to fail to make timely interest or principal payments. Rates on senior loans typically adjust with changes in prevailing short-term interest rates; therefore, when short-term rates rise, senior loan rates will rise and when short-term rates decline, senior loan rates will decline.

Real Assets are less developed, more illiquid, and less transparent compared to traditional asset classes. Real asset investments are subject to various risks generally associated with the ownership of real estate-related assets and foreign investing, including but not limited to, fluctuations in property values, higher expenses or lower income than expected, changes in economic conditions, currency values, environmental problems and liability, the cost of and ability to obtain insurance, and risks related to leasing of properties.

In addition to traditional equity risks like market risk or the risk that company values will decline in response to such factors as adverse company news, industry developments or a general economic decline, private equity investments involve significant risks specific to the asset class, including illiquidity, long investment horizons, capital call obligations, uncertain valuations, leverage/financing risk, and dependence on successful exits. Private equity investments are not publicly traded, making them difficult to value and sell.

The information contained is about the Nuveen target date strategies overall and also contains information about the Nuveen Lifecycle Income Index Collective Investment Trust Series described later on this presentation (Lifecycle CIT Series). Please note that the Lifecycle CIT Series is not a series of mutual funds and differs in many ways from the mutual funds using a similar strategy. Information about the mutual funds or management of the mutual funds should not be automatically applied to the CIT. The Lifecycle CIT series may be referred to as "Funds" in the following disclosures.

SEI Trust Company (the "Trustee") serves as the Trustee of the Nuveen Lifecycle Income CIT Series (the "Funds") and maintains ultimate fiduciary authority over the management of, and the investments made, in the Funds. The Funds are not mutual funds. The Funds are part of a Collective Investment Trust (the "Trust") operated by the Trustee. The Trustee is a trust company organized under the laws of the Commonwealth of Pennsylvania and wholly owned subsidiary of SEI Investments Company (SEI).

The Trust is managed by the Trustee based on the investment advice of Nuveen Fund Advisors, LLC, the investment adviser to the trust.

The Trust is a trust for the collective investment of assets of participating tax qualified pension and profit-sharing plans and related trusts, and governmental plans as more fully described in the Declaration of Trust. As a bank collective trust, the Trust is exempt from registration as an investment company.

Investing involves risk; principal loss is possible. There is no guarantee the Funds investment objectives will be achieved. The participant's conversion of some or all of their fixed annuity allocation to lifetime income benefits (i.e., annuitization) is a permanent decision, and once payments have begun, participants are unable to change to another option. TIAA may offer so-called "additional amounts" or "Loyalty Bonuses." The availability and amount of any additional amounts or Loyalty Bonuses is within the discretion of TIAA, they are determined annually and are not guaranteed other than for the period for which they are declared. Certain amounts or bonuses are only available when electing lifetime income, these amounts or bonuses are also discretionary and determined annually, and their amounts can vary depending on history of contributions to the fund. The terms of TIAA's Secure Income Account (SIA) specifically require that the SIA allocation generally cannot be rebalanced downward. So, if due to financial market movements or other forces, the SIA is overweighted versus target allocation, amounts generally cannot be removed from the SIA to correct the overweighting. Instead, the overweighting generally must be corrected through new cashflows into the fund. This represents a potential opportunity cost (because it may foreclose the ability to invest in higher earning equity investments for a period of time) and could thus impact performance of the fund over time. The performance of the fixed annuity component of the fund may be benchmarked against a bond index.

There are substantial differences between fixed annuities and the bond index, including differing investment objectives, costs and expenses, liquidity, safety, guarantees or insurance, and fluctuation of principal or return.

A plan fiduciary should consider the Funds' objectives, risks, and expenses before investing. This and other information can be found in the Declaration of Trust and the Funds' Disclosure Memorandum. The Fund is not a mutual fund, and its units are not registered under the Securities Act of 1933, as amended, or the applicable securities laws of any state or other jurisdiction.

TIAA Secure Income Account is a fixed annuity product issued through this contract by Teachers Insurance and Annuity Association of America (TIAA), 730 Third Avenue, New York, NY, 10017: Form series including but not limited to: TIAA-UQDIA-002-K, TIAA-STDFA-001-NUV and related state specific versions. Not all contracts are available in all states or currently issued. The TIAA Secure Income Account is approved for issuance in 52 of 53 U.S. insurance jurisdictions. It is not approved to be issued to New York-domiciled contract holders. Annuity contracts may contain terms for keeping them in force. We can provide you with costs and complete details. The TIAA Secure Income Account is a guaranteed insurance contract and not an investment for federal securities law purposes. Any guarantees under annuities issued by TIAA are subject to TIAA's claims-paying ability. Past performance is no guarantee of future results. Guarantees of fixed monthly payments are only associated with fixed annuities.

©2025 Teachers Insurance and Annuity Association of America-College Retirement Equities Fund, 730 Third Avenue, New York, NY 10017

Nuveen, LLC provides investment solutions through its investment specialists.

Nuveen and Economist Impact, or any of their affiliates or subsidiaries are not affiliated with or in any way related to each other. The research was independently developed by Economist Impact and is sponsored by Nuveen, LLC. This material is prepared by and represents the views of Economist Impact, and does not necessarily represent the views of Nuveen, its affiliates, or other Nuveen staff.

Contact us

Nuveen Retirement Investing sales desk

Please be advised, this content is restricted to financial professional access only.

Login or register as a financial professional to gain access to this information.

or

Not registered yet? Register

You are about to access our website for visitors outside of the United States.

You're about to access test site

You are about to access our website for Nuveen Global Cities REIT

You are leaving the Nuveen website.

You are leaving the Nuveen website and going to the website of the MI 529 Advisor Plan, distributed by Nuveen Securities, LLC.The Nuveen website for institutional investors is available for you.

You are about to access our website for visitors outside of the United States.

You are about to access our website for Nuveen Churchill Private Capital Income Fund (“NC - PCAP”)