0

Fund 1

Fund 2

Fund 3

Fund 4

Contact us

Contact Nuveen

Thank You

Thank you for your message. We will contact you shortly.

Retirement investing

Benefits 2.0 survey: looking to the future so your participants can focus on the present

A new era of financial pressure

Workers today are facing a period of sustained financial uncertainty, in which rising living costs, market volatility and job security concerns are reshaping how they balance immediate needs with long-term financial goals. With this in mind, Nuveen commissioned Economist Impact to conduct the second Benefits 2.0 survey, building on its 2023 research.1 The 2025 survey, with responses from more than 2,000 U.S. workers, examines how economic conditions are influencing career decisions, savings behavior and retirement expectations — and what these shifts mean for plan sponsors.

Key takeaways:

- Workers are increasingly concerned about rising costs of living and job security. They are taking steps to feel more secure, either by no longer looking for work or changing retirement contributions.

- Our respondents are pushing out their planned retirement dates, some due to health care costs, others due to fears around Social Security.

- There is a place for AI in benefits planning, as workers show a relatively high level of trust for AI agents and would let them be more involved in the process.

The findings point to a clear change in priorities. Younger and lower-income workers are increasingly willing to trade higher wages for greater stability and stronger benefits. At the same time, many employees are making short-term financial adjustments that will weaken their long-term retirement readiness. Together, these trends underscore the expanding role of employer-sponsored benefits in supporting workforce resilience. One indicative number was that 62% of U.S. workers say they would prefer long-term job security over higher pay or stronger benefits if those came with less security.

Workers are borrowing from their futures

Our survey also indicates that 51% of U.S. workers have taken or applied for a job with equal or lower pay in exchange for a more attractive benefits package throughout their careers, and 15% have done so in the past 12 months. This presents an opportunity for employers to use their overall benefits package to attract talent, while not necessarily having to offer significantly higher salaries at the same time.

Conversely, in the last 12 months, 30% of Gen Z report that they have stopped or delayed looking for a new job due to a fear of losing job security, compared to just 14% of all workers. Also reporting, 9.5% of millennials indicate lowering their retirement contributions in the last 12 months, again a sign of economic stress and uncertainty.

The pressure on those nearing retirement remains elevated across our results, with 7.5% of boomers Gen X workers saying that they have reduced their retirement contributions due to rising costs in the last year, while 6.6% have delayed retirement in the last 12 months.

The results of the survey also indicate that mid-career workers are most exposed, with around four in ten millennials (40%) and Gen X workers (39%) having accessed retirement savings early. This is troubling as early withdrawals from retirement savings can have a compounding effect for those with decades left in their careers. The survey also shows that more than one-third of millennials (37%) have reduced retirement contributions during their careers. These numbers lead us to recommend more educational resources be made available by employers to help show workers why they should try to keep retirement contributions stable through their highest earning years.

There is also a worrying statistic that could highlight a growing risk, with 8% of both higher and middle-income workers having reduced retirement contributions in the last 12 months alone. This could become worrying trend if it sets in and those workers don’t catch up with those contributions.

Retirement expectations pushed further out of reach

Retirement expectations have shifted as a result of ongoing cost of living increases, with respondents overall expecting to retire around four years later than they had originally planned. These expectations are shifted even more for lower-income workers (around six years) and workers with less than a college education (about five years).

21% of Millennials workers cite the potential for changes to Social Security as a reason why they might have to delay retirement. These shifting expectations for retirement offer an opportunity to plan sponsors to ensure that they have systems in place to build that confidence back up in their workers, whether through a lifetime income product or an alternative, to give participants increased confidence that when they do retire, they’ll be able to maintain the same standard of living.

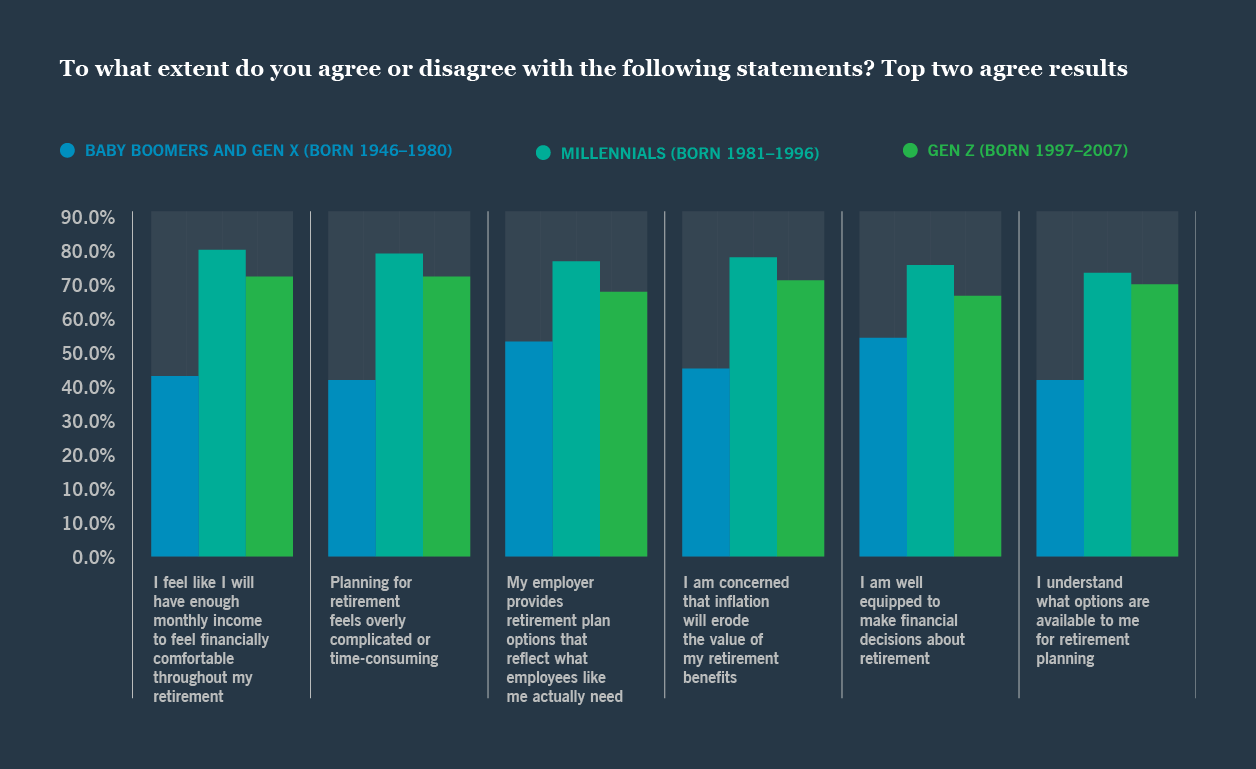

General understanding of retirement planning and options available is encouragingly high, with 72% of workers saying that they understand the retirement planning options available to them, but this number falls for certain demographics. Just 47% of Gen Z say that they understand their options, and only 52% of lower-income workers say the same. These demographics are the ones that would benefit from educational campaigns to boost their knowledge of available options. One number that could be cause for concern is the 70% of respondents who say that planning for retirement feels overly complicated or time-consuming.

It is also of note that nearly two-thirds of workers (63%) say that they made initial retirement choices but rarely review or change them. While this can be seen as a relatively positive point for a plan that is well-constructed, we would like to make sure that advice and engagement are available for participants as their expectations for retirement shift throughout their careers. The survey shows that disengagement in reviewing retirement plans is highest among millennials (69%), junior staff (77%) and low- to middle-income workers (71%).

A surprising level of enthusiasm for AI in benefits

One rapidly growing area of retirement planning is the potential for AI advice and modeling. With these tools growing in sophistication all the time, they may be a way for plan sponsors to mitigate the expense of customized advisory services while still helping employees feel engaged.

The survey showed that overall, 70% of workers trust their employer to use AI to personalize benefits based on employee data. Specifically, 77% of millennials and 61% of Gen Z trust their employer to use AI in this way, and with these generations having the longest runway left before retirement this could be a way to change behaviors at a relatively early stage. Perhaps even more surprisingly, 66% trust employers to use AI to help decide which benefits to add or cut, showing a level of willingness to outsource difficult and complex decisions to AI models to relatively new technology.

However, there are some qualifiers to this trust. Four in ten (39%) cite data privacy as one of their three biggest concerns. Three in ten (30%) worry about biased or inaccurate AI recommendations and 26% fear AI could replace human support. But there was mitigation, with 48% saying that they are more likely to use AI tools if there are better data protections in place, and 40% say that they would be more confident using these tools with a human alongside the AI.1

There are some other concerns from participants that would need to be resolved as well, with 26% of respondents citing limited knowledge of how to use AI tools effectively as one of their top worries, and 23% offering a perception that AI tools are too complicated to use properly.

Re-centering benefits in a volatile world

In summary, the 2025 Benefits 2.0 survey highlights a workforce under sustained financial pressure. In response, many workers are prioritizing stability, adjusting savings behavior and seeking long-term security at the expense of postponing retirement.

At the same time, engagement and knowledge gaps continue to limit workers’ capacity to adapt effectively. These challenges elevate the role of employer-sponsored benefits as a critical source of stability, guidance and confidence.

By investing in thoughtful plan design, targeted education and technology-enabled support, sponsors can meaningfully help employees navigate uncertainty during these challenging times. For sponsors, delivering accessible, personalized and trustworthy retirement solutions will be central to improving outcomes for today’s workforce.

For sponsors, delivering accessible, personalized and trustworthy retirement solutions will be central to improving outcomes for today’s workforce.

Continue reading

Explore a principles-based framework for adding guaranteed lifetime income to TDFs without losing sight of their core purpose.

A principled approach

to TDFs with guaranteed

lifetime income

Explore now

TIAA Institute research finds that hybrid retirement systems with integrated guaranteed income offer the best path to lasting retirement security.

Addressing the retirement

conversion challenge:

a global perspective

Explore now

Nuveen makes the case for embedding private market investments within target-date funds to broaden diversification and improve retirement outcomes.

The next frontier

for defined

contribution:

embedding

private assets

Explore now

*Any guarantees are backed by the claims-paying ability of the issuing company. Past performance is no guarantee of future results. Guarantees of fixed monthly payments are only associated with fixed annuities.

**The ability to annuitize is subject to plan rules. Converting/Exchanging some or all of your savings to income benefits (referred to as "annuitization") is a permanent decision. Once income benefit payments have begun, you are unable to change to another option.

There is no guarantee that an investment in a target date fund will provide adequate retirement income at or through retirement and investors can lose money at any stage of investment, even near or after the target date.

Asset allocation and diversification do not ensure a profit or protect against a loss. Be sure to see the relevant prospectus or offering document for full discussion of a target date investment option including determination of when the portfolio achieves its most conservative allocation.

Before investing, carefully consider fund investment objectives, risks, charges and expenses. For this and other information that should be read carefully, please request a prospectus or summary prospectus from your financial professional or Nuveen at 800.257.8787 or visit nuveen.com

This material, along with any views and opinions expressed within, are presented for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as changing market, economic, political, or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. There is no promise, representation, or warranty (express or implied) as to the past, future, or current accuracy, reliability or completeness of, nor liability for, decisions based on such information, and it should not be relied on as such. This material should not be regarded by the recipients as a substitute for the exercise of their own judgment. It is important to review your investment objectives, risk tolerance and liquidity needs before choosing an investment style or manager.

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell or hold a security or investment strategy and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor's objectives and circumstances and in consultation with their financial advisors. Financial professionals should independently evaluate the risks associated with products or services and exercise independent judgment with respect to their clients.

This material does not constitute a solicitation of an offer to buy, or an offer to sell securities in any jurisdiction in which such solicitation is unlawful or to any person to whom it is unlawful to make such an offer. Moreover, it neither constitutes an offer to enter into an investment agreement with the recipient of this document nor an invitation to respond to it by making an offer to enter into an investment agreement.

This material may contain "forward-looking" information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of yields and/or market returns, and proposed or expected portfolio composition. Moreover, certain historical performance information of other investment vehicles or composite accounts managed by Nuveen may be included in this material and such performance information is presented by way of example only. No representation is made that the performance presented will be achieved, or that every assumption made in achieving, calculating or presenting either the forward-looking information or the historical performance information herein has been considered or stated in preparing this material. Economic and market forecasts are subject to uncertainty and may change based on varying market conditions, political and economic developments. Any changes to assumptions that may have been made in preparing this material could have a material impact on any of the data and/or information presented herein by way of example.

Important information on risk

Past performance is no guarantee of future results. All investments carry a certain degree of risk, including the possible loss of principal, and there is no assurance that an investment will provide positive performance over any period of time. Certain products and services may not be available to all entities or persons. There is no guarantee that investment objectives will be achieved. See the applicable product literature for details.

Investors should be aware that alternative investments are speculative, subject to substantial risks including the risks associated with limited liquidity, the potential use of leverage, potential short sales, currency exchange rates, and concentrated investments and may involve complex tax structures and investment strategies. Alternative investments may be illiquid, there may be no liquid secondary market or ready purchasers for such securities, they may not be required to provide periodic pricing or valuation information to investors, there may be delays in distributing tax information to investors, they are not subject to the same regulatory requirements as other types of pooled investment vehicles, and they may be subject to high fees and expenses, which will reduce profits.

Target Date Funds: The principal value of the fund(s) is not guaranteed at any time, including at the target-date. The value of a target date fund will fluctuate and investors may lose money. There is no guarantee the Funds' investment objectives will be achieved. For example, it may not achieve its target allocations and even if it does, the asset allocations may not achieve the desired risk-return characteristics and may result in the fund underperforming other similar funds. The target date is an approximate date when investors may begin withdrawing from the Funds. Target-date funds are actively managed, so the asset allocation is subject to change and may vary from that shown. Also, once the target date has been reached, the Funds may be merged into another with the same asset allocation or possibly another with a more stable asset allocation. For Index Funds, a portfolio that tracks an index is subject to the risk that it may not fully track its index closely due to security selection and may underperform when factoring in fees, expenses, transaction costs, and the size and timing of shareholder purchases and redemptions. Target date funds are typically fund of funds subject to the risks of their underlying funds in proportion to each Funds' allocation. These risks may include those of fixed-income underlying funds risks, such as market risk, credit risk, interest rate/duration risk, call risk, tax risk, political risk, economic risk, and income risk. Typically the value of, and income generated by, fixed income investments will decrease or increase based on changes in market interest rates. As interest rates rise, bond prices fall and as interest rates fall, bond prices rise. The Funds' income could decline during periods of falling interest rates. Income is only one component of performance and investors should consider all of the risk factors for an asset class before investing. Credit risk refers to an issuer's ability to make interest and principal payments when due, as well as the prices of bonds declining when an issuer's credit quality is expected to deteriorate. Equity underlying funds risks are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Non-U.S. investments involve risks such as currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards.

Real estate-related assets are less developed, more illiquid, and less transparent compared to traditional asset classes. Real estate investments are subject to various risks, including but not limited to, fluctuations in property values, higher expenses or lower income than expected, changes in economic conditions, currency values, environmental problems and liability, the cost of and ability to obtain insurance, and risks related to leasing of properties.

Private credit/debt investments, like alternative investments are not suitable for all investors given they are speculative, subject to substantial risks including the risks associated with credit risk, interest rate risk, currency risk, prepayment and extension risk, inflation risk, and risk of capital loss, limited liquidity, the potential use of leverage, potential short sales, concentrated investments and may involve complex tax structures and investment strategies. Credit risk refers to an issuer's ability to make interest and principal payments when due, as well as the prices of loans declining when an issuer's credit quality is expected to deteriorate.

Adjustable-Rate Senior Loans may not be fully secured by collateral, generally do not trade on exchanges, and are typically issued by unrated or below-investment grade companies and therefore are subject to greater liquidity and credit risk. Lower credit debt securities may be more likely to fail to make timely interest or principal payments. Rates on senior loans typically adjust with changes in prevailing short-term interest rates; therefore, when short-term rates rise, senior loan rates will rise and when short-term rates decline, senior loan rates will decline.

Real Assets are less developed, more illiquid, and less transparent compared to traditional asset classes. Real asset investments are subject to various risks generally associated with the ownership of real estate-related assets and foreign investing, including but not limited to, fluctuations in property values, higher expenses or lower income than expected, changes in economic conditions, currency values, environmental problems and liability, the cost of and ability to obtain insurance, and risks related to leasing of properties.

In addition to traditional equity risks like market risk or the risk that company values will decline in response to such factors as adverse company news, industry developments or a general economic decline, private equity investments involve significant risks specific to the asset class, including illiquidity, long investment horizons, capital call obligations, uncertain valuations, leverage/financing risk, and dependence on successful exits. Private equity investments are not publicly traded, making them difficult to value and sell.

The information contained is about the Nuveen target date strategies overall and also contains information about the Nuveen Lifecycle Income Index Collective Investment Trust Series described later on this presentation (Lifecycle CIT Series). Please note that the Lifecycle CIT Series is not a series of mutual funds and differs in many ways from the mutual funds using a similar strategy. Information about the mutual funds or management of the mutual funds should not be automatically applied to the CIT. The Lifecycle CIT series may be referred to as "Funds" in the following disclosures.

SEI Trust Company (the "Trustee") serves as the Trustee of the Nuveen Lifecycle Income CIT Series (the "Funds") and maintains ultimate fiduciary authority over the management of, and the investments made, in the Funds. The Funds are not mutual funds. The Funds are part of a Collective Investment Trust (the "Trust") operated by the Trustee. The Trustee is a trust company organized under the laws of the Commonwealth of Pennsylvania and wholly owned subsidiary of SEI Investments Company (SEI).

The Trust is managed by the Trustee based on the investment advice of Nuveen Fund Advisors, LLC, the investment adviser to the trust.

The Trust is a trust for the collective investment of assets of participating tax qualified pension and profit-sharing plans and related trusts, and governmental plans as more fully described in the Declaration of Trust. As a bank collective trust, the Trust is exempt from registration as an investment company.

Investing involves risk; principal loss is possible. There is no guarantee the Funds investment objectives will be achieved. The participant's conversion of some or all of their fixed annuity allocation to lifetime income benefits (i.e., annuitization) is a permanent decision, and once payments have begun, participants are unable to change to another option. TIAA may offer so-called "additional amounts" or "Loyalty Bonuses." The availability and amount of any additional amounts or Loyalty Bonuses is within the discretion of TIAA, they are determined annually and are not guaranteed other than for the period for which they are declared. Certain amounts or bonuses are only available when electing lifetime income, these amounts or bonuses are also discretionary and determined annually, and their amounts can vary depending on history of contributions to the fund. The terms of TIAA's Secure Income Account (SIA) specifically require that the SIA allocation generally cannot be rebalanced downward. So, if due to financial market movements or other forces, the SIA is overweighted versus target allocation, amounts generally cannot be removed from the SIA to correct the overweighting. Instead, the overweighting generally must be corrected through new cashflows into the fund. This represents a potential opportunity cost (because it may foreclose the ability to invest in higher earning equity investments for a period of time) and could thus impact performance of the fund over time. The performance of the fixed annuity component of the fund may be benchmarked against a bond index.

There are substantial differences between fixed annuities and the bond index, including differing investment objectives, costs and expenses, liquidity, safety, guarantees or insurance, and fluctuation of principal or return.

A plan fiduciary should consider the Funds' objectives, risks, and expenses before investing. This and other information can be found in the Declaration of Trust and the Funds' Disclosure Memorandum. The Fund is not a mutual fund, and its units are not registered under the Securities Act of 1933, as amended, or the applicable securities laws of any state or other jurisdiction.

TIAA Secure Income Account is a fixed annuity product issued through this contract by Teachers Insurance and Annuity Association of America (TIAA), 730 Third Avenue, New York, NY, 10017: Form series including but not limited to: TIAA-UQDIA-002-K, TIAA-STDFA-001-NUV and related state specific versions. Not all contracts are available in all states or currently issued. The TIAA Secure Income Account is approved for issuance in 52 of 53 U.S. insurance jurisdictions. It is not approved to be issued to New York-domiciled contract holders. Annuity contracts may contain terms for keeping them in force. We can provide you with costs and complete details. The TIAA Secure Income Account is a guaranteed insurance contract and not an investment for federal securities law purposes. Any guarantees under annuities issued by TIAA are subject to TIAA's claims-paying ability. Past performance is no guarantee of future results. Guarantees of fixed monthly payments are only associated with fixed annuities.

©2025 Teachers Insurance and Annuity Association of America-College Retirement Equities Fund, 730 Third Avenue, New York, NY 10017

Nuveen, LLC provides investment solutions through its investment specialists.

Nuveen and Economist Impact, or any of their affiliates or subsidiaries are not affiliated with or in any way related to each other. The research was independently developed by Economist Impact and is sponsored by Nuveen, LLC. This material is prepared by and represents the views of Economist Impact, and does not necessarily represent the views of Nuveen, its affiliates, or other Nuveen staff.

Contact us

Financial professionals

Individual investors

You are on the site for: Financial Professionals and Individual Investors. You can switch to the site for: Institutional Investors or Global Investors

Please be advised, this content is restricted to financial professional access only.

Login or register as a financial professional to gain access to this information.

or

Not registered yet? Register

You are about to access our website for visitors outside of the United States.

You're about to access test site

You are about to access our website for Nuveen Global Cities REIT

You are leaving the Nuveen website.

You are leaving the Nuveen website and going to the website of the MI 529 Advisor Plan, distributed by Nuveen Securities, LLC.The Nuveen website for institutional investors is available for you.

You are about to access our website for visitors outside of the United States.

You are about to access our website for Nuveen Churchill Private Capital Income Fund (“NC - PCAP”)